Historically, fulfillment partners focused on outbound operations: shipping speed, order accuracy, and delivery reliability. Returns were considered a secondary issue to manage, rather than a core capability to assess.

This perspective no longer applies in markets with high e-commerce return rates. In Germany and the UK, returns are now significant enough to redefine what brands require from logistics partners. When a substantial portion of shipments are returned, fulfillment partners must be as proficient with inbound operations as they are with outbound.

This article outlines the requirements high-return-rate markets place on fulfillment operations and how to assess whether a partner is equipped to meet them.

Table of Contents

The Return Rate Reality in Germany and the UK

Germany has one of the highest e-commerce return rates in Europe. Fashion and apparel returns often exceed 40%, with some subcategories even higher. This is driven by a well-established consumer behavior: German shoppers frequently order multiple sizes or variants, intending to return items that do not fit. Known as bracketing, this is a mainstream purchasing pattern that retailers in Germany must accommodate in their logistics planning.

The UK also experiences high return rates, with apparel returns ranging from 25% to 35%, remaining elevated even as other European markets have moderated. The competitive fast fashion sector and strong consumer protection, supported by the Consumer Rights Act 2015, foster expectations of easy returns and frequent use of this right.

The EU Consumer Rights Directive, implemented across Germany and all EU member states, provides consumers with a 14-day right of withdrawal on distance purchases. In Germany, this baseline is often exceeded by retailers who voluntarily extend it to 30 days to remain competitive. What this means operationally: any brand selling into Germany should design its reverse logistics around 30-day return windows as the effective standard, not the legal minimum.

These patterns have substantial financial implications. For example, a brand shipping 5,000 orders per month to Germany with a 35% return rate processes 1,750 returns monthly. Each return incurs inbound shipping, warehouse receiving, inspection labor, restocking or disposition, and often a refund within a set timeframe. At £10–15 per return, this results in £17,500–26,000 in monthly reverse logistics costs, excluding inventory that cannot be restocked and capital tied up in returns.

What This Means for Fulfillment Partner Requirements

In high-return-rate markets, evaluating fulfillment partners shifts from focusing solely on outbound performance to assessing their ability to manage both outbound and inbound operations effectively.

This shift redefines which partner capabilities are most important.

Returns Processing Speed as a Core SLA Parameter

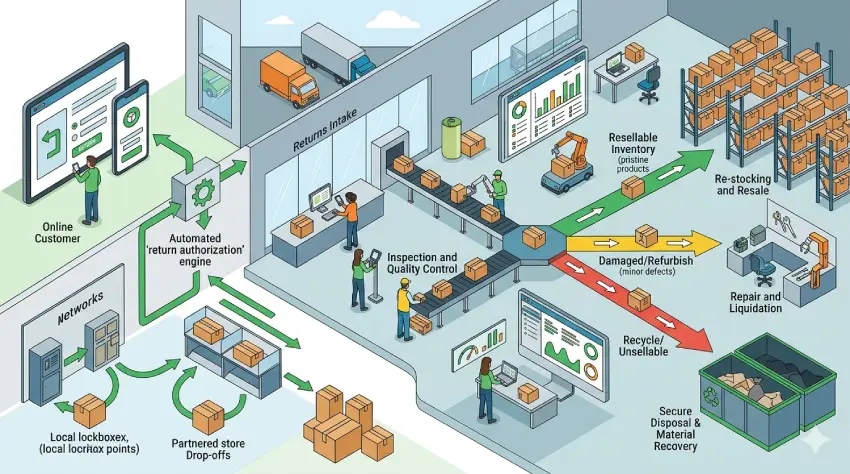

In low-return-rate markets, return processing time is often loosely defined or overlooked. In Germany and the UK, it must be a clearly defined and measured SLA, as processing speed directly impacts two key brand priorities.

First, refund timelines. German and UK consumers expect prompt refunds, and platforms such as Amazon DE hold sellers accountable for refund speed through performance metrics. Delays in inspection and refund processing can lead to increased customer service inquiries, negative reviews, and potential penalties.

Second, inventory recovery. Once a returned item is inspected and deemed resaleable, it should be promptly returned to available stock. Delays in this process result in phantom inventory—items physically present but unavailable for sale—which can significantly impact inventory accuracy at high return volumes.

The recommended SLA for fulfillment partners in Germany or the UK includes: inspection of returned items within 24–48 hours of receipt, back-to-stock decisions and inventory updates within the same timeframe, and refund initiation for resaleable items within this window. These are operational standards, not aspirational goals, in high-return markets.

Inspection Depth and Product-Specific Criteria

A generic inspection—simply checking for damage—is inadequate for most high-volume product categories. Brands in Germany and the UK increasingly require product-specific inspection criteria, defined in advance and consistently applied at the warehouse.

For fashion, criteria include: is the garment unworn, are tags intact, is the original packaging present and resaleable, and are there any signs of use such as deodorant marks, makeup transfer, or fabric pilling that would make the item non-resaleable? These standards should be documented and not left to individual discretion.

Under German law, the standard is stricter: any product with a broken hygienic seal cannot legally be resold, regardless of apparent use. Inspection processes must verify seal integrity to be compliant.

For electronics, inspections must include functional testing for relevant product types, not just visual checks. Failing to identify non-functional items can result in repeat returns, increased handling costs, and negative reviews.

When evaluating a fulfillment partner for Germany or the UK, ask how product-specific inspection criteria are documented, stored, and implemented by warehouse staff. Relying on individual judgment does not provide the consistency required for high-volume inspections.

Disposition Logic Beyond Binary Resell/Discard

In high-return markets, a simple “resell or discard” approach often overlooks value. Many returned items are lightly used, have minor cosmetic damage, or lack original packaging but remain fully functional.

What these items need is a third path: secondary channel routing, refurbishment, or markdown pricing. These items require alternative disposition options such as secondary channel routing, refurbishment, or markdown pricing with clear condition disclosure. Brands in Germany increasingly use outlet channels, open-box categories, or B-stock listings on platforms like the Zalando Partner Program to recover value from such returns for items that aren’t going directly back to primary stock. This might mean repackaging with a condition-graded label, routing to a separate secondary inventory location, or flagging for brand review before a disposition decision is made. Partners who can only offer a binary outcome are limiting the brand’s value recovery options.

Return Volume Surge Capacity

Germany’s e-commerce calendar includes predictable return volume spikes that fulfillment operations must address. The post-Christmas period, especially the first two weeks of January, sees return volumes at three to four times the weekly average for fashion. Additional spikes occur after Prime Day, Black Friday, and major promotions.

A fulfillment partner that manages standard return volumes but cannot handle surges risks operational failures. Backlogs in January can delay refunds, increase customer service demands, and leave inventory unavailable during key sales periods when markdown pricing is most effective.

To evaluate surge capacity, ask how return volumes were managed during the first two weeks of January, what the average processing times were compared to normal weeks, and whether temporary staff were used. If so, inquire how inspection standards are maintained with less experienced workers.

The Cross-Border Dimension: Returns from Germany and the UK to a Centralized Warehouse

Brands fulfilling from a single warehouse in Germany, the Netherlands, or elsewhere in Europe face reverse logistics challenges when selling cross-border. Returns must be shipped back to the fulfillment point, which may be outside the customer’s country.

Since Brexit, UK-based sellers must address new customs requirements for international returns. German customers returning products to UK fulfillment centers may incur customs charges, and UK brands may face import duties on returns from Germany, depending on value and product type. These issues affect all cross-border returns.

A practical solution for brands with significant volume in both Germany and the UK is to provide local return addresses in each country, with periodic consolidation to the primary fulfillment warehouse. This approach eliminates customs complexities, lowers customer return shipping costs, and improves processing speed.

For brands working with a fulfillment partner that has physical infrastructure in Germany, these brands benefit from local collection points. German customers return items to a local facility, where products are inspected and either restocked locally or consolidated to the main warehouse. Brands lacking this infrastructure must absorb or pass on cross-border costs, creating friction in high-return markets. A framework for brands operating in Germany, the UK, or both:

Return processing time: What is the defined SLA for completing inspections after returns arrive? Is this metric tracked, reported, and contractually enforced? Request actual performance data from the last quarter, not just stated targets.

Product-specific inspection: Can inspection criteria be set at the brand or SKU level and recorded in the warehouse management system? How are these communicated to staff, and how is consistency ensured, especially with temporary workers during peak periods?

Disposition options: Does the partner support more than two disposition paths? What infrastructure is in place for secondary channel routing, condition grading, or repackaging? What is the process for items that do not meet standard resell criteria?

Surge capacity: How did return processing times change during the most recent January surge and post-promotion periods? How does the partner staff for surges, and how are quality standards upheld with temporary workers?

Local returns infrastructure: Does the partner have a physical presence in Germany and the UK? Can local return addresses be provided in each market? How is consolidation from local return points to primary inventory managed?

Inventory visibility: Are returned items visible in inventory systems in real time or with a delay? Can brands track the status of in-transit returns before warehouse arrival? Does the platform distinguish between in-transit, received pending inspection, and inspected back-to-stock statuses?

Refund trigger workflow: Who initiates refunds—the brand, the fulfillment partner, or an automated process based on inspection status? What is the average time between inspection completion and refund initiation?

The Broader Shift

The developments in Germany and the UK illustrate the broader evolution of e-commerce. As markets mature and consumer expectations around returns become established, reverse logistics shifts from a cost center to a strategic capability. Brands that adapt early and select fulfillment partners accordingly gain lasting advantages: improved inventory accuracy, faster refunds, greater value recovery, and a returns experience that strengthens brand trust.

Brands that do not recognize this shift continue to assess fulfillment partners mainly on outbound metrics, only to encounter challenges as return volumes increase. This often leads to renegotiations or transitions under operational pressure, making change more difficult.

The evaluation framework applies whether a brand is selecting its first European fulfillment partner or reviewing an existing one. In both scenarios, returns management deserves equal attention to outbound operations, as it is equally critical to success in Germany and the UK.